History Predicts Rates to Increase by 5% over the Next 2.5 Years

May , 2015

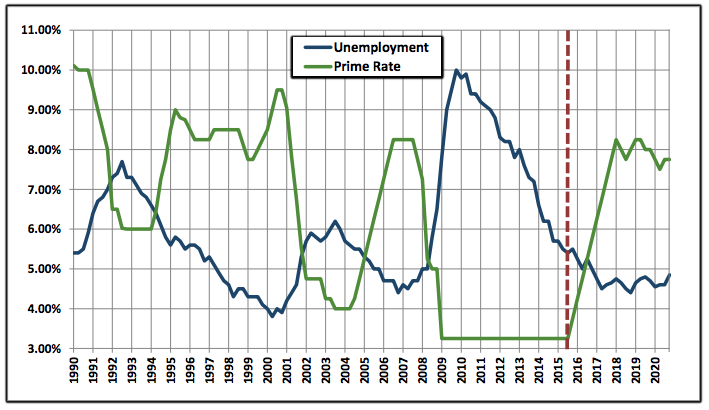

Don’t get caught in the rising tide. With unemployment rates dipping below 6% and showing no signs of stopping, experts say it is only a matter of time before the Fed begins taking steps to increase interest rates. Those with variable rate loans would be wise to lock in the current low market interest rates by refinancing with a long-term fixed interest rate loan product.

The charts below say it all. Historic interest rates have generally moved conversely with unemployment rates as the Fed balances economic activity to stabilize prices and moderate long-term interest rates. Since 1990, there have been two significant periods of increases in the prime interest rate as outlined below. In both instances, the prime rate increased significantly each quarter until reaching a level between 8% and 9%. If history repeats itself, we can expect the prime rate to increase by 5% over the next 30 months.

Rate Increase

Time Period

Duration

Increase Per Qtr.

3.00%

Jan ’94 – March ’95

15 Months

0.60%

4.25%

April ’04 – June ’06

27 Months

0.47%

5.00%

July ’15 – Dec ’17

30 Months

0,50%

With a 40%+ drop in the unemployment rate since 2010, and the unemployment rate already in the target range of 5-6%, most experts expect to see interest rates begin increasing in the late second quarter of this year.

A recent article in the New York Times stated:

“The Federal Reserve on Wednesday moved to the verge of raising interest rates for the first time since the economy fell into recession more than seven years ago… In a statement released after a two-day meeting of its policy-making committee, the Fed said that it would consider raising its benchmark rate as early as June, and it removed from the statement a promise that it would be “patient.”… [Yellen’s] remarks suggested that borrowers have a few more months to take advantage of exceptionally low interest rates on mortgages and car loans.”

Locking in one of your largest expenses as a small business owner – your monthly debt payment. With so many variable expenses, certainty is certainly desirable.

Dramatically reducing your monthly debt payment by extending your loan term to 10 years. Many have increased their free cash flow by as much $3,000 per month by extending their loan term. It is important to note that with PPCLOAN, you can always make additional payments to reduce your outstanding principal without penalty.

Tapping into the equity of your Franchise by securing working capital to further grow your business through implementing new marketing initiatives, hiring additional staff, office expansions, etc.

For over 17 years PPCLOAN has consistently provided the most attractive financing programs available for small business owners across the country. With PPCLOAN you can expect quality service and tailored financing solutions for refinancing your existing business loan as well as for acquisitions (internal & external), mergers, partnership buy-ins and buy-outs, and succession plans. Put our knowledgeable and experienced staff to work for you and experience the difference!

In life you are either facing your problems or turning your back on them as if they did not exist. Unfortunately, the reality is that problems do exist and they don’t just go away unless they are dealt with. If you are not dealing with your problems as they arise you will be buried by them as they accumulate unresolved.

Your past is always going to be there. If you are dealing with your past problems, your future doesn’t stand much of a chance. The best place for the past is in the past. In this context, success can be defined as effectively handling the affairs of life. Deal with your affairs whether good or bad, and move on.

Here are some positive steps to take in solving life’s problems as they arise.

Realize, and more importantly accept, that you have a problem. If you find that you are having trouble zeroing in on your problem, remember, that which weighs on you the most usually is the problem.

Recognize that you are the only one that can solve the problem. Though others can help, no one else can do it for you.

Focus on solutions. Focusing on and rolling around in the problem is like driving down the road while looking in the rearview mirror. You will ultimately pile misery upon misery.

When life hands you a pile of problems prioritize. Deal with the “A” and leave the remainder of the list alone, when the “A” is solved the “B” becomes “A”. Change what you can change and move on.

Dealing with your problems as they come upon you involves a forward looking approach to life. A healthy exercise to stay forward looking is to make a list and contemplate your blessings. Remember what you take for granted is many times a blessing.

One of the most common challenges we all face in life is some type of financial problem. Virtually all financial problems have one thing in common: they get worse if left unaddressed. This means that if you get into financial difficulty, don’t bury your head in the sand.

Financial problems boil down to two basic sides of the equation – how much is coming in, and how much is going out. Therefore, the inevitable solution to financial problems involves improving one or both sides of the equation. Ask the typical person what will help resolve his financial turmoil and you will almost always get the same answer: “More Money.” Unfortunately, most money problems are caused by poor money management habits and skills (rather than a lack of money). When money management skills are weak, increasing the supply of money is rarely the solution. Case in point, the U.S. is full of professionals with six-figure incomes who have no savings and live paycheck to paycheck.

When faced with problems involving debts consider the answers to the following questions in order to gain a complete understanding of your situation:

Exactly how much do you owe right now?

Who do you owe it to?

When do you have to pay?

Does the lender or creditor offer a payment plan?

Have you talked to the creditor or lender about options?

What are the consequences of not paying?

How soon will this crisis be over?

Debts fall into two categories, secured and unsecured. Secured liabilities are guaranteed by property, either real or personal. A mortgage is a secured debt. An auto loan is a secured debt. Credit card balances are the most common example of unsecured debt. List all your debts and determine which category each of your debts falls under. When you are in a financial crisis, the payment order for your bills should be determined by their importance in sustaining and maintaining your life. Keep in mind that, if you don’t make the payments on a secured debt, the creditor can ultimately take control of the property used for collateral on the loan.

Stay in touch with your lenders. They are in this with you and can only help if they know there is a problem, and you need to know what actions they are or may be planning to take. Many people avoid talking with their lenders out of fear that the lender will automatically “lower the boom” on them. However, aggressive steps such as foreclosure are NOT the first course of action a lender will usually take. In fact, foreclosure is a long and expensive process for lenders and that often results in a loss for them. Lenders prefer you to keep your home and/or business. Thus, most lenders will first look to temporary solutions which may include reduced payment plans, forbearance, and workout packages.

Solving financial problems requires that you understand the underlying cause of the crisis. Examine the reasons objectively. If you have health issues, loss of employment, or have sustained damages from a natural disaster, there are agencies that can help you. Do some research and don’t be afraid or embarrassed to ask for help. If your money problems are a result of poor management or overspending, don’t berate yourself. Maintaining your self-esteem and a positive attitude will enable you to make good rational decisions so you can work your way out of debt.

Look for ways to reduce the amount you pay out each month. Trimming the fat from your budget requires diligence and sacrifice. Pack a lunch, give up smoking, use grocery store coupons, and search out free entertainment. Learning to save and live more frugally can be a giant step towards financial stability.

Filing bankruptcy, while always an option, should be viewed as the option of last resort, and should not be pursued until stability in one’s income and spending habits have been achieved. This means the decision to file for bankruptcy shouldn’t be based on a strategy focused on dealing with the debts you’ve built up, but rather on a strategy based on emerging with a better future. To do otherwise is to ensure that you will emerge from bankruptcy headed for the same financial troubles all over again.

Unfortunately, bad things do happen to good people. And sometimes these bad things involve your personal financial situation. The next time you face a financial crisis take a few calming breaths, and remember, you are not in it alone and you will get through it.

About the author: K.M. “Mac” Winston is president and chief lending of PPC LOAN, L.L.C., a Texas‐based provider of bank financing that serves the professional marketplace nationwide. Mac has over 25 years of banking experienceand has specialized in lending to service sector professionals since 1992. Mac can be contacted at (800) 456‐2779 or [email protected].